Smartphone growth acceleration in China drives demand, but turmoil in Brazil has lead to declining smartphone sales in Latin America, according to new global research.

Global smartphone demand hit 368m units in Q4 2015, up 14 percent quarter-on-quarter and up six percent year-on-year, according to new research.

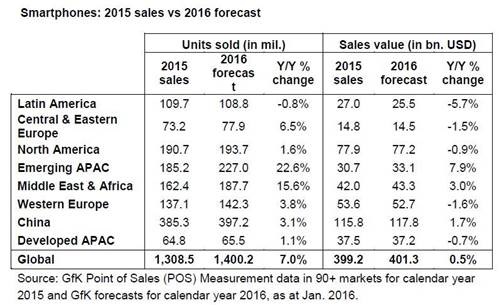

The research, from GfK, looks at smartphone penetration in over 90 markets around the world during January 2016.

Key findings include:

However, revenues plateaued year-on-year at US$115bn due to average selling price (ASP) declines of six percent year-on-year for Q4 2015. In the full year 2015, 1.3bn smartphone units were sold, an increase of seven percent year-on-year. However, this unit growth was partially offset by a decline in global average selling price (ASP) of two percent year-on-year, which caused revenues to increase on a slightly lower level of only five percent year-on-year to US$399bn.

Kevin Walsh, director of trends and forecasting at GfK comments, “Despite a record fourth quarter – and a strong performance in 2015 in general – there are mixed results across countries. Local factors, rather than regional and industry trends, are increasingly driving markets. Diverging economic trends, device saturation, mass market adoption, politics, social change and even sport have an impact on smartphone demand and prices at country level.”

Emerging APAC: a growth powerhouse

Emerging APAC remains the primary growth driver in the global smartphone market, with 21 percent year-on-year unit growth in Q4 2015.

On a country level, India is a key driver with unit growth of 34 percent year-on-year, driven by its dominant low-end (sub-US$100) price band segment, which saw unit growth accelerate to 76 percent year-on-year. There is still plenty of room for smartphone demand from first time buyers, since penetration of the sub-US$100 segment stood at only 24 percent in the last quarter of the year.

China: growth accelerated in Q4 2015

After a return to a moderate growth in 3Q 2015 (following a series of four negative quarterly year-on-year developments that started in 3Q 2014), China saw smartphone growth accelerate to 12 percent year-on-year in 4Q 2015. In this period a record high of 106.6m units was reached. With a volume growth of 11m units, China contributed half of the global growth in the last quarter.

The shift towards LTE-enabled, larger-screen devices continues. 5”+ handsets accounted for 71 percent of smartphones sold in the quarter, up from 53 percent in the same period of 2014. LTE-enabled smartphone share has almost reached saturation levels. GfK forecasts unit growth will slow to 17 percent in 2016, considerably down from 248 percent in 2015. Competitively priced local brands continue to gain share in the country, accounting for 75 percent of smartphone demand in Q4 2015, up from 69 percent in Q4 2014.

GfK forecasts a return to moderate growth of three percent in China in 2016 – following the two percent year-on-year decline seen in 2015. This is likely to be helped by an expected increase in operator subsidies.

MEA: Egypt is the star performer

Despite a slight slow-down in growth, smartphone unit demand in the MEA grew 12 percent year-on-year in the quarter. Most countries in the region saw increases, but Egypt stood out with demand growing 27 percent year-on-year.

Latin America: Consumers move towards low-end devices

Smartphone demand in Latin America continued to decline in Q4 2015, dropping 13 percent year-on-year. This was dragged down by macroeconomic weakness in Brazil, which caused demand to decline 26 percent year-on-year in the country. ASP in the region declined 12 percent year-on-year as a result of a shift in consumer preference towards low-end devices. This fall in demand, combined with the lower ASP, resulted in a revenue drop of 23 percent year-on-year to US$7bn.

Developed APAC*: overall demand is stable

Unit demand in Developed APAC remained stable in Q4 2015 following a three percent year-on-year decline in the previous quarter. Smartphone demand in South Korea returned to growth (up eight percent year-on-year) for the first time since Q4 2013. This was helped by easy comparisons with the weak performance in Q4 2014. However, regional growth was offset by a six percent decline in year-on-year demand in Japan.

Western Europe: growth in France, Germany and Great Britain

Smartphone unit growth in the region stood at five percent year-on-year in Q4 2015, helped by 61 percent year-on-year growth in the ultra-low-end (sub-US $100) segment. Overall growth accelerated in its three largest markets: France, Germany and Great Britain.

Central Europe: mild growth driven by Poland

Smartphone unit growth in Central Europe remained limited at four percent year-on-year, but was helped by strong growth of 36 percent year-on-year in Poland. Due to political and economic issues, year-on-year demand in Russia and Ukraine dropped seven percent and 14 percent respectively.

Kevin Walsh explains, “In 2016, we expect local country factors rather than global trends to impact the market. Key markets in Emerging Asia and Middle East & Africa are forecast to drive unit growth. While 2016 will be another year of global growth, it will be more important than ever for businesses to understand individual country trends and market segments.”