The UK ad market is forecast to contract by £4.2bn (16.7%) this year) to £21.1bn this year due to the coronavirus lockdown and economic slump.

The figures were revealed in the Advertising Association/Warc Expenditure Report, which is regarded as one of the industry’s most authoritative surveys.

The report predicts that the second quarter from April to June 20202 will see a crash og 39.1%, and indicates that every medium is facing double-digit declines.

Even previously high-growth sectors such as internet search and online display are predicted to suffer badly in the second quarter, down by 29.6% and 31.8% respectively.

TV is forecast to fall 46.6%, radio 44.1%, national news brands 45.3%, out-of-home 52.6% and cinema 100%.

Full-year figures in the new Advertising Association/WARC Expenditure Report show UK adspend rose 6.9% year-on-year to reach £25.36bn in 2019. And while 2020 started promisingly, the downgrading of projections for the rest of the year demonstrate the deep impact that COVID-19 has had on advertising since mid-March, as it has the UK economy as a whole.

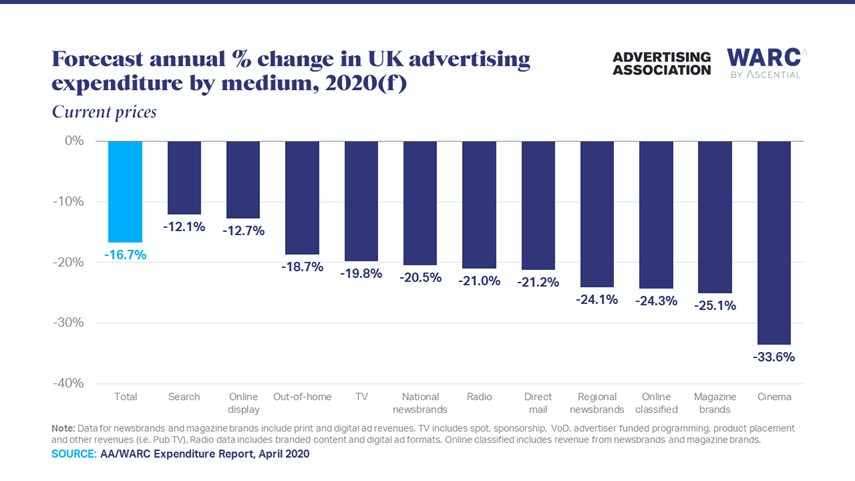

Projections prior to the COVID-19 outbreak forecast adspend growth in 2020 of 5.2% to a total of over £26bn. The revised forecast is for advertising expenditure of £21.13bn meaning a year-on-year reduction of 16.7% – or £4.23bn – from 2019. Adspend is expected to return to growth in 2021 with a rise of 13.6%, but absolute levels of investment are not expected to surpass the 2019 total.

Online formats performed strongly during the past year and they are forecast to decline by less than traditional formats during 2020. Search and social media – 45.7% of the UK ad market combined – grew by 17.8% and 24.6% respectively in 2019 but are predicted to fall by 12.1% and 6.3% respectively this year – the first recorded declines in these sectors.

Broadcaster video on demand (VOD) recorded growth of 15.5% in 2019 but, overall, TV saw a decline of 3.5%. Both are expected to be affected by the downturn this year, with TV forecast to see a 19.8% dip in advertiser investment and VOD a 6.3% fall.

The ongoing decline in publisher revenue that was recorded in 2019 is expected to intensify this year, with decreases of 20.5% for national newsbrands, 24.1% for regional newsbrands, and 25.1% for magazine brands. All are then expected to record growth in 2021.

Given the restrictions on population movement and gathering ordered by the Government, the out of home and cinema markets are expected to see large falls in adspend in 2020, with growth projections at -18.7% and -33.6% respectively. However, cinema and digital out of home are forecast to recoup losses fully in 2021 – the only channels to do so.

The second and third quarters will take the biggest hit

Rates of decline range from 27.2% for broadcaster VOD to 52.6% in the out of home market during the second quarter. The forecasts do not anticipate cinemas to open their doors before July, resulting in spend drying up completely.

Overall, the market is expect to contract by 39.1% – or £2.4bn – during the second quarter of 2020, while spend is projected to fall by a further 24.3% in Q3.

“This virus-induced recession is different to previous downturns in that the impact has been both swift and sharp across all media,” said James McDonald, Head of Data Content, WARC.

“The deterioration of advertising trade, we believe, will be focused primarily in the second and third quarters of this year, though the aftershocks are likely to last into the fourth quarter and early 2021.”

He singled out the effects of the lockdown on small and medium sized enterprises for whom digital advertising – paid search especially – is a staple and whose recovery is expected to take some time.

“Media costs have fallen as a direct result of lower demand for inventory and this, paradoxically, comes at a time when consumption and reach has grown markedly across TV, social media and online publications,” McDonald added.

“Research on WARC from multiple sources shows that cutting advertising in a recession directly correlates with a slower recovery, but the practicalities of marketing in the current climate mean sustained investment is simply no longer feasible for a number of large product sectors.”

The UK advertising industry response

The Advertising Association is working with partners across advertising on innovative plans to boost adspend and reactivate growth in the market. One of the actions being called for is a tax credit scheme for advertising and marketing services, with the aim of stimulating investment and encouraging advertisers to continue, or return to, advertising,.

Such a plan would also encourage companies that do not currently advertise, typically SMEs, to invest in advertising. It would also act as a stimulus for the wider economy and provide a welcome boost in investment for British commercial media.

The Advertising Association is also calling for other measures to rebuild confidence in the market, for example:

• A phased-down extension of the Job Retention Scheme when lockdown ends, to avoid a wave of redundancies by companies with cashflow problems.

• Priority to be given to the advertising production sector to allow it to start up again as soon as possible and to ease its transition from lockdown. Production has virtually stopped and by its nature it requires human presence so there will need to be new arrangements around social distancing.

• Government to provide support in the credit insurance markets to ensure that cover limits offered to agencies are sufficient to allow all those UK advertisers who want to advertise to do so without constraint in this respect.

Stephen Woodford, Chief Executive, Advertising Association commented “Despite a good 2019 and promising start to 2020, COVID-19 has affected UK advertising as it has all parts of the economy and the falls we are seeing in adspend come as little surprise. The current quarter will be a tremendously tough time for many businesses across our industry. We are acutely conscious of their predicament and working fast with Government and officials, so that they get the best support possible.

The Advertising Association welcomed Monday’s Government announcement on Bounce Back Loans which will help keep small businesses afloat. It would also like to see an extension of the business rates relief to the advertising sector, and relief on commercial rents for tenants.

Industry comment

Richard Wright, Head of Marketing, Scoro, said: “The £4.23bn reduction in the revised 2020 forecast for ad spend will be setting off alarm bells at media agencies across the country. Widespread budget shaving measures to brace business for the storm are already being widely reported and while expectations for 2021 growth are positive, many are concerned about what the near future has in store.

“To weather this difficult time, efficiency will be key for agencies. Remote-working throws up new challenges for teams, but it also presents a good opportunity to re-evaluate what best practice should be. Time is money and now is the time to invest in, and innovate with, tools and techniques for effective collaboration to give agencies that much-needed boost in 2020, and a springboard into a more productive 2021.”

Rachel Powney, VP of Marketing, Dugout, said: “The ad spend forecasts for 2020 reflect how companies are rethinking marketing strategies in response to changing consumer behaviour. Despite blanket keyword blocking weighing on forecasts as brands seek safe haven from COVID-19 related content, the report highlights a leap in online traffic of between 30% and 60% for premium publisher sites, with consumers locked down and hungry for news, entertainment and sports – which does present advertisers with an opportunity.

“We have already seen some industries like food, financial services and DIY suppliers adapt their strategies to focus on mission-based and cause-based marketing, to tap into consumer needs according to their situation. With a touch of creativity and a focus on contextual relevance, bolder brands have an opportunity to corner the market and make the best of a challenging 2020.”

Chris Hogg Managing Director EMEA, Lotame, said: “Advertisers that push ahead with adspend in the next few months will be at a competitive advantage post-pandemic. Lower programmatic CPMs, less competition from brands who are not advertising and more consumers online presents an opportunity to gain market share growth now and be in a strong position for the upturn.

“This is a good time to learn about and build a panoramic view of the customer, test creative messages and optimise data enrichment strategies. With more people at home and increased eyeballs on screens there is also the scope to advertise in new environments you wouldn’t typically consider. News sites, for example, have seen a huge surge in readership but also a reluctance from some brands to advertise due to the Covid context – providing the messaging is right and socially conscious, opportunities are present.”

Ali MacCallum, CEO Kinetic UK, said: Even in the toughest period that any of us can remember, out of home has continued to demonstrate its power to get influential communications out to audiences immediately and publicly.

“In recent months OOH has played a key role in delivering vital public information right across the country. While none of us anticipated the day that OOH would be used as a medium to urge people to stay indoors, we’ve still seen some brave and brilliant campaigns from the likes of Tesco and Paddy Power as well as some fantastic initiatives supporting our key workers – often amplified at scale via social media. It is this dynamic creativity that will be positively remembered as we start to return to some form of normality.

“There is growing optimism that the market will start to pick up in the coming weeks and months. As restrictions are gradually lifted OOH will have a crucial role to play in the UK’s social and economic recovery. The smart deployment of dynamic digital OOH will become highly effective for brands looking to reach audiences across location and context to communicate that they are open for business, and to capitalise on the demand that has built up.

“This period has taught us all of the simple joy of being out of home. As the country moves out of lockdown, OOH can begin to move back towards the upward trajectory that we have seen in recent years.”

David Fletcher, Chief Data Officer at Wavemaker, said: “While the short-term outlook is extremely challenging, we share the longer-term optimism that the market will return to growth.

“A lot of the current commentary is based on the old playbooks about brands continuing to invest through recession, however the current situation is far more complex than just an economic downturn. Decisions brands take now will determine how well placed they are to get back on the path to growth.

“At Wavemaker we talk a lot about brands being not just present but present with purpose. Even in unprecedented circumstances, there are brands that have strengthened their relationship with existing and potential customers. It’s not simply that they have invested, it’s that they have put their investment in the right place, while demonstrating humanity and generosity that has resonated with the public”.

Sam Taverner, EVP, Merkle EMEA, said: “Inevitably the short-term picture is extremely challenging. The forecasts point to a significant negative adjustment in ad spend in Q2 with hospitality and travel spend halted completely. However, some of that difference will be made up by increased government spending and continued strength in online retail, media and telecommunications.

Nevertheless there is a growing consensus that we will start to see a return to some form of normality later this year. Even when restrictions start to ease, the outlook is complex and constantly evolving as we adjust to the ‘new normal’. Businesses would be well advised to divert their budget to data science and planning, in preparation for optimising the expected ramp-up in spend in Q3. In fact, many are already using this period of enforced pause to their advantage, using deep analytics to re-evaluate large swathes of their strategy and to develop more robust ad- and mar-tech foundations.

“Agility will be crucial as businesses look to bounce back. The use of data to properly inform new strategies and business plans and to drive a host of decisions across businesses at pace will be critical, not just to short-term survival, but to long-term growth.”

Claire Burgess, Head of Biddable, NMPi by Incubeta, said: “We saw similar trends which match the findings of the AA/WARC ad spend report – a great 2019 and start to 2020 until COVID-19 hit, which has caused clients to review their ad spend. While online has been performing well for the majority of industries, most retailers are holding back as they compensate for overheads from brick and mortar stores.

“With concern that footfall and revenue will never return to previous levels, clients will need to meticulously plan the future of their stores. We expect to see a huge shift in the way clients use their budgets as they try to claw back sales by turning to digital as consumers become more accustomed to buying online.

“While this report calls out supporting small and medium-sized businesses (SMBs) through credits, I would also expect to see a focus on online-only businesses who, on the whole, are performing well and are increasing spend. Despite the fact that large companies will be seeing huge decreases in spend, if this report was broken out to show SMBs and online-only businesses, we would be seeing a very different trend.”

Ben Little, Founder and Director at Fearlessly Frank comments:“‘All models are wrong, but some are useful’ is a famous quote by the statistician George Box. It’s relevant in our COVID-19 dominated times, as beneath every model are assumptions and ‘best guesses’ as to what might happen to other variables when one changes. Therefore unless the assumptions made to prepare these forecasts are made evident, this forecast is at best a wet finger held in the air.

“The global economy is going through something we have never seen before. The scars and consequences will change behaviours and limit expenditure for years to come; what happens to advertising next will be determined by how advertisers think they can take advantage of a depressed market. The changes in consumer behaviour will be impossible to predict, and so we must feel our way back to a different business growth model.

“As an innovation business, we have already spoken to multiple organisations who are concerned that they have failed to innovate at pace, in favour of security. Now that this security has gone, they’re left scrabbling with diminished resources and little room for manoeuvre. Innovation will be key to survival in a post COVID-19 world.”

Paps Shaikh, Commercial Director – EMEA at Nextdoor comments: “The downturn in the AA/WARC ad spend forecast for the rest of 2020 and 2021 is to be expected. Covid-19 has impacted on the whole of the advertising industry as well as that of the wider UK economy.

“Yet, as a rebound is expected in 2021, with a return to growth of 13.6%, this will only be achievable if brands remain bullish and advertise their way through this period to ensure they are front of mind when normality resumes. To do this they must keep an open dialogue with consumers and keep the narrative going, as retreating will only leave a void to be filled by others.

“While media channels across the board are experiencing a decline in spending, brands need to be savvy and tweak their strategy to ensure they are making the most of the different channels available to them. Platforms, such as social media, can do just this, by enabling brands to have meaningful conversations with their target audience in real-time.”